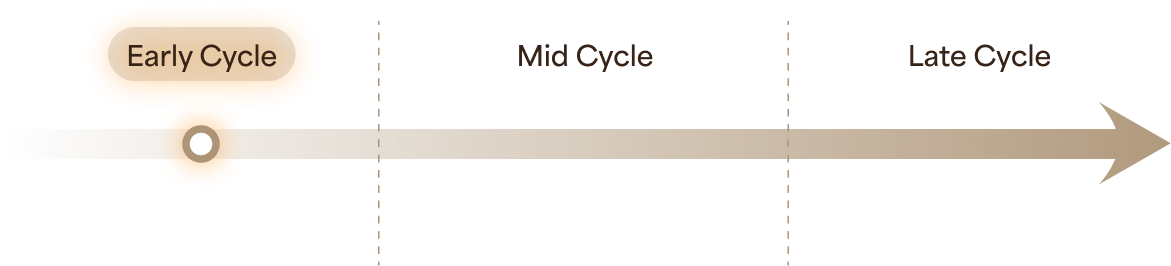

Catching the right cycle

We position capital ahead of economic and industry cycles, where risk-reward is most asymmetric.

Earnings growth and valuation re-rating phase

Identifying the right

promoters (owner-operators)

We back promoters who behave like long term owners because sustainable compounding begins with credible stewardship.

Promoter Evaluation Framework

Capital Allocation Discipline

Avg RoCE above cost of capital across cycles

Minority Shareholder Treatment

Simple structures, clean disclosures, limited off-balance-sheet risk

Balance sheet Prudence

Moderate leverage, cash flows over reported margins

Decision-making under stress

Rational reallocation during downturns, not value-destructive defence

Alignment of Interests

Meaningful ownership and long-term skin in the game

Promoters are evaluated by behavior over time, not narratives is in favorable cycles.

Risk Management Process

Risk management is embedded at every stage of our investment process, not treated as an afterthought.

Supporting Investment Lenses

Alongside our core philosophy, we continuously monitor a set of supporting factors that help sharpen timing, risk assessment, and portfolio positioning.

- Industry inflection points that alter competitive dynamics

- Earnings and margin recovery signals indicating improving business quality

- Capital cycle and policy shifts that reshape supply, demand, and returns

These lenses help us participate early in opportunities while avoiding late-cycle excesses.

CATCHING THE NEXT CYCLE

What Is The Opportunity?

01

We are agnostic Growth/Value Tags - Oppotunistic in nature

We do not anchor portfolios to predefined styles. Capital is deployed where the expected return justifies the risk, whether emerging from growth inflections, mispriced quality, or cyclical recoveries

02

We are Market Capitalization Agnostic - Allocation based on core fundamentals

We invest across large, mid, and select small-cap companies where business quality, governance, and valuation converge.

03

We are conscious about not overpaying for any Business

Even exceptional businesses can deliver poor outcomes if acquired at excessive valuations. We seek a margin of safety by aligning price with long-term earnings potential.

04

Purposeful thinkers when it comes to making investment decisions - Remain invested as long as the thesis is valid

We are not married to our positions and remain invested as long as the original thesis remains intact. Our stocks don’t know that we own them.

05

We believe in a basket approach to capitalize on opportunities in India

Our investments fit into baskets like cycle plays, shift (promoter/segment/capital allocation), stable compounders, high growth but optically expensive and pre-ipo opportunities with a pre-defined weight range assigned to each allocation in a basket.

Basket Approach

5-7% Allocation

Cycle Plays

HDFC Bank | Northern Arc | IIFL Finance | Shyam Metallics | Borosil Renewables

3% Max Allocation

Shift Basket (Promoter/Segment/ Capital Allocation)

Wockhardt | Panacea | Tanfac | Tega Industries

4-5% Allocation

Stable Compounders

Shriram Piston | Sundaram Fastners | Happy Forging | VST Tillers

5% Allocation

High Growth but optically expensive

Ami Organics | SKF | Craftsman | Sansera Engineering

2% Max Allocation (Exited)

Pre IPO Investments

Environ Infra | Exicom Telesystems

What Do We Avoid ?

- In Companies

- In Investing

In Companies

Hot stocks or concept stocks

Businesses that we do not understand

Expensive valuations

Promoters with corporate governance issues

Leveraged companies/promoters

In Investing

Forecasting the markets

Investing on the basis of technical analysis

Churning the portfolio

Following the herd